BUFFALO, N.Y. (WKBW) — When Pastor George Nicholas steps outside his church in Buffalo’s Masten District, he sees a steady stream of cars making their way down Main Street.

But what Nicholas is really looking at is Buffalo’s invisible dividing line.

To the west is the Elmwood Village, a majority-white area where the medium household income is $51,000 per year. Nardin Academy, Canisius High School and the Saturn Club are less than a mile away.

East of Main Street is where 85 percent of Black Buffalonians live. There -- in a U.S. Census tract roughly the same geographic size as three tracts on the west of Main -- the median household income is just $24,000 per year.

“There’s almost been this acceptance of this as, ‘Oh, that’s just the way Buffalo is,” said Nicholas, pastor of Lincoln Memorial United Methodist Church.

But this stark disparity did not happen organically. If it seems that people looked at a map and drew lines down Main Street dividing the “haves” from the “have nots,” it’s because they did.

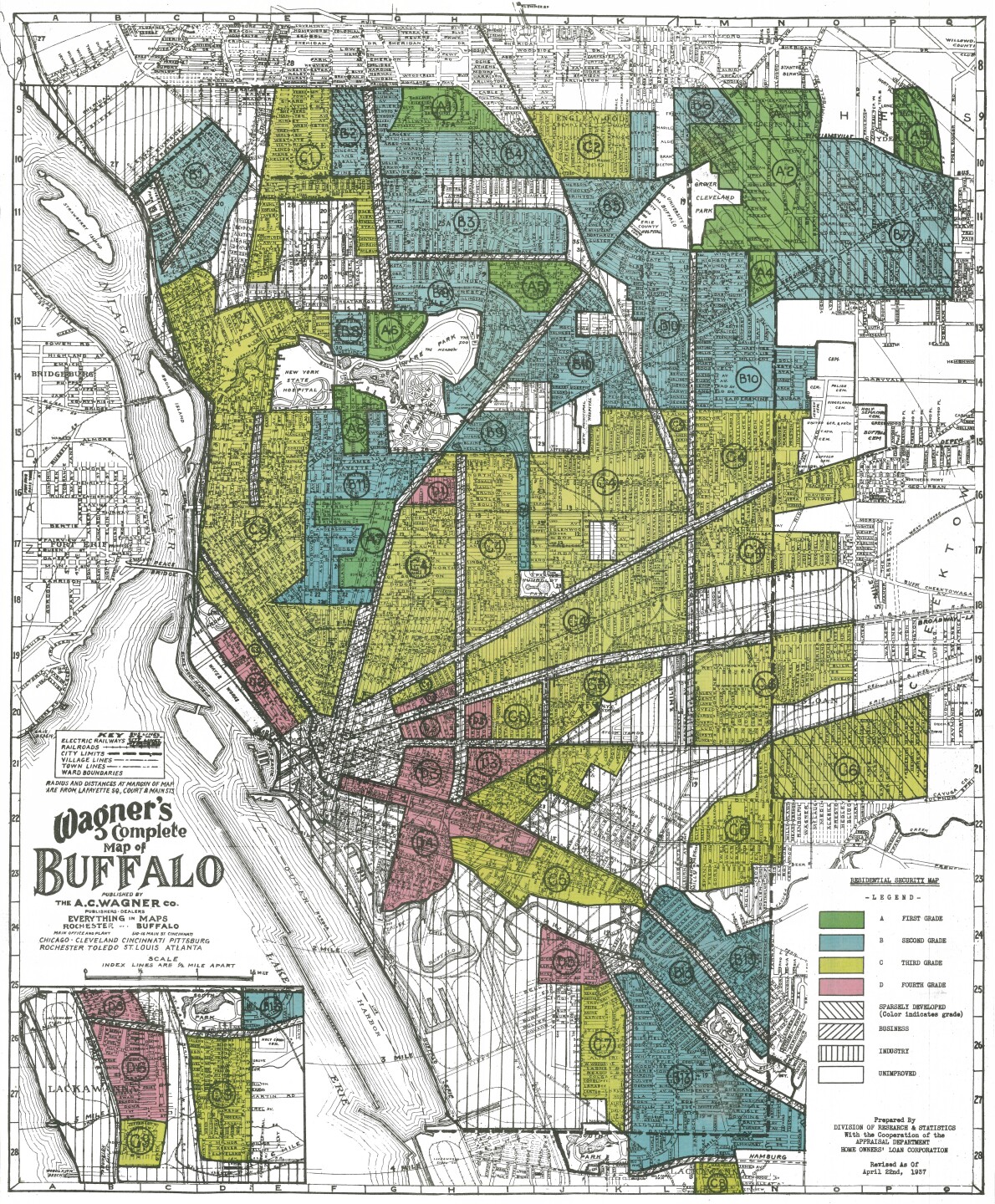

Maps drawn in 1937 for the Home Owners’ Loan Corporation -- a federal government agency -- were used by the mortgage industry for decades to deny mortgages in areas where poor people and residents of color lived, a practice known as “redlining.”

“So the federal government created these maps all around the country, these underwriting maps, and they said, ‘Here's where we'll underwrite mortgages and encourage them and here's where we'll discourage them,’” said Sam Magavern, senior policy fellow at the Partnership for the Public Good, a Buffalo nonprofit organization.

Click here to see the full interactive map.

How Buffalo was redlined

The maps -- published online as part of the “Mapping Inequality” project between the University of Richmond, University of Maryland, Johns Hopkins University and Virginia Tech -- were color-coded by the level of “mortgage security” that HOLC staff and local real estate professionals estimated in those areas.

Areas shaded in green -- that meant Delaware Avenue, pockets of North Buffalo and some of the region’s first suburbs -- were deemed “best” for mortgage lending because they had “many magnificent homes on large plottages which are still being maintained by the leading families of Buffalo.”

But any sort of ethnic diversity was a drawback in the eyes of appraisers.

For instance, the western part of Elmwood -- on Ashland and Lafayette Avenues -- was downgraded by one level to blue because mapmakers warned that there was an “infiltration of mixed races” beginning to take place.

A large swath of Buffalo’s East Side running from downtown to the Cheektowaga line along Genesee Street was shaded yellow, meaning the mapmakers determined it to be “definitely declining.”

The area was on a “general downward trend through infiltration of lower income groups and foreign born,” they wrote.

One thing the area had going for it, the mapmakers stated, was the ethnicity of its residents: mostly Polish and German, which they described as “a substantial type of citizen.”

But a few blocks to the south -- an area stretching from Broadway down to where Sahlen Field now stands -- is shaded not yellow, but red. That area was deemed a “hazardous” place for bankers to lend, in part because of what officials deemed the “type of occupant.”

“An extremely old section which has been taken over by Italians and Negros of a poor type,” the map reads.

Nicholas’ church sits on the edge of the Cold Springs area, which -- unlike the majority-white neighborhoods bordering it on all sides -- was redlined and deemed “hazardous” for mortgage lending because of what mapmakers called the “infiltration” of Black people.

“It was the institutionalization of white privilege,” said Henry Louis Taylor Jr., director of the Center for Urban Studies at the University at Buffalo.

Taylor said the maps and banking practices that followed were based on an inherently racist economic principle created by the real estate industry and sanctioned by the government.

“Blacks drive value down,” he said, describing the thinking of the time. “Since Blacks drive value down, the secret to creating white value is by isolating them from Blacks.”

Economic and social impact

In a country in which owning your own home is one of the most common ways to build equity, the effects of such policies were devastating, academics and community leaders say.

“It impacts the ability to acquire wealth and the ability to transfer wealth, which is the American dream,” Nicholas said.

More than 80 years later, such blatantly racist policies have changed. But the disparities in wealth that they enabled are striking.

The Urban Institute in 2018 said Buffalo had the third-highest homeownership gap in the nation, with 73% of white people owning their own homes compared with just 29% of Black people.

“It's the single biggest reason that there's such a huge wealth gap in this country where the average white family has about 10 times the net wealth of the average African-American family,” Magavern said. “Ten times. That's a huge, huge difference.”

Redlined neighborhoods on Buffalo’s East Side entered into a spiral of disinvestment where “the lack of hope and opportunity creates a whole ‘nother set of issues,” Taylor said.

Neighborhoods of color differ from predominantly white neighborhoods in how likely residents are to be exposed to pollution, live near a highway, be surrounded by blight and vacancy, be underserved by banks, and have less access to supermarkets, according to the UB Regional Institute.

Researchers who digitized the redlining maps have also found significant ties between neighborhoods of color that were redlined and those that were disproportionately affected by the Covid-19 pandemic.

“These places, they kill people,” Taylor said. “Because they cause unnecessary disease, death, and dying.”

A thing of the past?

For decades, it has been illegal for banks to deny loans to people based on characteristics such as race, color or religion. The 1977 Community Reinvestment Act forced banks to provide much of their lending data for public inspection.

The 7 Eyewitness News I-Team analyzed data reported by banks to the federal government under the Home Mortgage Disclosure Act. That data showed that in 2020, loan applications of Black people in Erie County were denied at twice the rate of loan applications of white people.

When Black people applied for loans, they were denied 27 percent of the time, the data showed. When white people applied for loans, they were denied 12 percent of the time, according to the data, which the government collects from all financial institutions in Western New York.

Banks, though, have argued that those disparities can’t alone be attributed to racial discrimination, since Black Americans on average earn less than whites. The Center for Investigative Reporting did a statistical analysis of federal mortgage data and found that Buffalo was not one of the 58 worst cities it identified.

But twice in the last six years, Western New York banks were accused of racial discrimination in their mortgage business. In 2014, Evans Bank was sued by the State Attorney General for excluding a large swath of Buffalo’s East Side from its service area. Bank officials denied that racism was a factor.

“Evans has systematically denied its residential mortgage lending products and services to African-Americans in the Buffalo metro area,” prosecutors wrote. The bank settled with the AG in 2015, agreeing to create an $825,000 settlement fund to promote homeownership and affordable housing.

Evans Bank now ranks first in the Buffalo Niagara region in lending to majority-minority tracts, according to a report from the state Department of Financial Services that covered the period from 2016 to 2019.

“After defending our good name for over a year as a small community financial institution with limited resources, we agreed to a settlement without acknowledging any wrongdoing,” Evans spokeswoman Kathleen Rizzo Young wrote in an email. She declined an on-camera interview request about the bank’s efforts on the East Side. Click here to read Evans' full statement.

The state earlier this year also reached a settlement with Hunt Mortgage Corp., which it accused of “poor performance in lending to minorities” and “weaknesses” in its fair lending and compliance programs.

State officials said they found no evidence that Hunt, which agreed to develop a special financing program for properties located in majority-minority neighborhoods, intentionally discriminated based on race.

Changing the narrative

In non-minority neighborhoods, “there’s no sign that says Black people can’t live here,” Nicholas said. “It’s just become part of the culture.”

Some banks are making aggressive efforts to change that culture. In 2018, KeyBank opened a branch at the corner of E. Delavan Avenue and Grider Street.

“We identified that there was a hole in services on the East Side of Buffalo,” said Kawanza A. Humphrey, a senior vice president at KeyBank.

Humphrey, who grew up on the East Side, said the bank actually has five other branches that serve that part of the city, and has invested in affordable housing and workforce training.

The bank holds financial education sessions on Saturday mornings aimed at increasing financial literacy in underserved communities and has also invested more than $40 million on projects related to job training and affordable housing on the East Side, Humphrey said.

The day the E. Delavan branch opened in a vacant former Rite Aid, neighbors stopped in to thank KeyBank officials for putting down stakes, she said.

“I cannot tell you of any community that has provided a warmer welcome for us,” Humphrey said. “We're just pleased to be able to make those types of investments in people and families in this community.”

M&T Bank has also made investments on the East Side by supporting Westminster Charter School and the Buffalo Promise Neighborhood. M&T recently received an "outstanding" rating from the federal government on its adherence to the Community Reinvestment Act, which tracks lending in communities of color.